Microsoft (MSFT 2.10%) hasn't had a great start to 2026. Its stock recently was down 11% for the yearwith the bulk of that fall coming after its second-quarter fiscal year 2026 earnings reportwhen it declined 10% in a single day.

This decline will make it difficult to outperform the market in 2026as the stock doesn't get the benefit of starting at its current low price tag. It must make up the ground it has lost. The S&P 500 (^GSPC +0.00%) is up a mere 1%so it doesn't have a ton to make up. Stillit won't be easy for Microsoft.

HoweverI think there's one clear reason why Microsoft can still outperform the market in 2026and it all revolves around Azure.

Image source: Getty Images.

Cloud computing is the key to AI

Azure is Microsoft's cloud computing division. Cloud computing plays a huge role in AIas upstarts and developers cannot afford to build a massive data center filled with the necessary computing equipment to train and run an AI model properly. Insteadbig tech companies like Microsoft are building excess computing capacitythen renting it to their clients. As long as Microsoft can build the data centersbuy the expensive computing unitsand then operate them for less than what they chargeit's a huge opportunity for Microsoft.

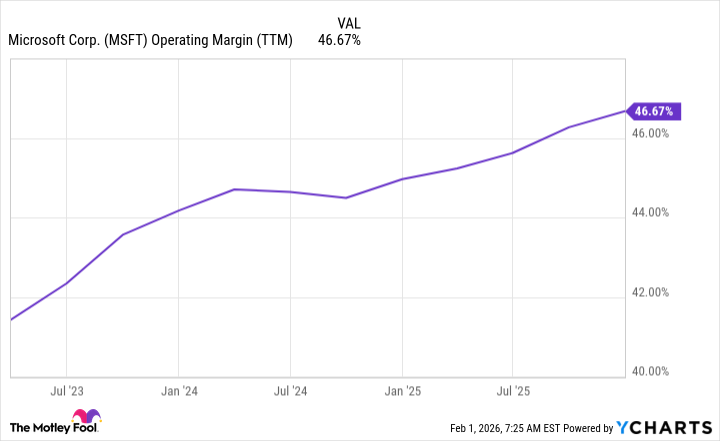

Unfortunatelywe don't know what the economics of Azure's business arebecause Microsoft doesn't individually break out its profits by division. Howevertwo of Azure's competitorsAmazon Web Services (AWS) and Alphabet's Google Clouddo. During the first quarterAWS delivered a 35% operating margin. Google Cloud's operating margins were 24% during the same period.

So I think it's safe to assume that Azure's operating margins are likely within 25% to 35%. Compared to Microsoft's overall operating margin of around 47%this means that Azure could be a drag.

MSFT Operating Margin (TTM) data by YCharts.

HoweverAzure's operating margin may be better than its peers'. There's just no way to be certain. RegardlessAzure is Microsoft's fastest-growing segmentincreasing its revenue at a 39% pace during Q2 (ended Dec. 312025). Management also noted that Azure's growth rate could have been faster if it had used the computing capacity that came online during Q1 and Q2 for external use rather than internal.

Microsoft's overall growth rate for Q2 was 17%. The next-fastest-growing segment was Microsoft 365 Consumer Cloud at 29% growth. Clearlycloud computing is leading the way for Microsoftand I think it will continue to do so for many years. Microsoft can still rise to outperform the broader marketand if it doesit will be because of its cloud computing platform.