How will asset tokenization transform the future of finance?

< data-emotion="wef 1jvs0wc">.chakra .wef-1jvs0wc{line-height:var(--chakra-lineHeights-tall);font-size:var(--chakra-fontSizes-large);color:var(--chakra-colors-black);font-weight:var(--chakra-fontWeights-bold);}

Asset tokenization could open up the financial markets to everyone Image: Getty Images/iStockphoto

< data-emotion="wef spn4bz">.chakra .wef-spn4bz{transition-property:var(--chakra-transition-property-common);transition-duration:var(--chakra-transition-duration-fast);transition-timing-function:var(--chakra-transition-easing-ease-out);cursor:pointer;text-decoration:none;outline:2px solid transparent;outline-offset:2px;color:inherit;}.chakra .wef-spn4bz:hover,.chakra .wef-spn4bz[data-hover]{text-decoration:underline;}.chakra .wef-spn4bz:focus-visible,.chakra .wef-spn4bz[data-focus-visible]{box-shadow:var(--chakra-shadows-outline);}Sandra Waliczek

< data-emotion="wef 1c50r5i">.chakra .wef-1c50r5i{line-height:var(--chakra-lineHeights-tall);font-size:var(--chakra-fontSizes-smaller);font-weight:var(--chakra-fontWeights-bold);color:var(--chakra-colors-greyDark);font-:normal;}Blockchain and Digital Assets, < data-emotion="wef 1yw72cb">.chakra .wef-1yw72cb{line-height:var(--chakra-lineHeights-tall);font-size:var(--chakra-fontSizes-smaller);font-weight:var(--chakra-fontWeights-normal);color:var(--chakra-colors-greyDark);font-:normal;}World Economic Forum- < data-emotion="wef 2uxndz">.chakra .wef-2uxndz{font-weight:var(--chakra-fontWeights-bold);color:var(--chakra-colors-black);line-height:var(--chakra-lineHeights-tall);}.chakra .wef-2uxndz a{color:var(--chakra-colors-blue);text-decoration:none;}.chakra .wef-2uxndz a:hover{text-decoration:underline;}

- The financial markets are undergoing a quiet revolution powered by asset tokenization.

- Asset tokenization could make investing more accessiblefastercheaper and more transparent.

- When institutionsregulators and tech providers come together to build trustedinteroperable frameworkswe are likely to see asset tokenization fulfil its potential.

Recent developments in US regulation following the GENIUS Act have put digital assets in the headlines. This regulation is focused on digital currencybut the next phase of digital assets is focused on asset tokenization.

In an increasingly digital worldthe financial markets are undergoing a quiet revolutionone that promises to make investing more accessiblefastercheaper and more transparent.

This revolution is powered by asset tokenizationa concept that leverages blockchain technology to digitize and fractionalize ownership of real-world assetslike stocksbonds and real estate.

While the idea of digital assets may bring to mind volatile cryptocurrenciesasset tokenization is something quite different and arguably more transformative for global finance.

Not to be confused with digital paymentsat its coretokenization has the potential to increase access to financial markets via opening up ownership of previously inaccessible assetsparticularly for retail investors and people in emerging economies who have found it difficult to access traditional financial institutions.

The World Economic Forum recently published the Asset Tokenization in Financial Markets: The Next Generation of Value Exchange reportwhich takes a deep dive on this topic.

What is asset tokenization?

Asset tokenization is the process of creating a digital representationcalled a "token"of a real-world asset on a distributed ledger or blockchain. These tokens are programmabletraceable and can be transferred peer-to-peer.

Each token acts as a digital certificate of ownership or a claim to a portion of an asset. For exampleinstead of buying a whole share in a private company or an entire commercial buildinginvestors can buy fractions of that asset represented as tokens. These tokens can be traded on blockchain-based systemspotentially 24/7 and globally.

Breaking down the benefits

Asset tokenization offers several potential advantages over traditional financeespecially in terms of accessibilityefficiency and transparency.

1. Democratizing financial market access

One of the most powerful promises of tokenization is its ability to level the playing field for retail investors and those in developing markets. Historicallyinvesting in certain asset classeslike private equityreal estate or commoditieswas reserved for institutional players or high-net-worth individuals due to high capital requirementsregulatory barriers and limited access to global markets.

Tokenization changes this by enabling asset fractionalizationbreaking assets into smallermore affordable units. Someone in Bangkokfor instancecould buy a token representing a share in a Bangkok office building. This radically lowers the barriers to entryenabling broader participation in wealth-building opportunities.

In emerging economieswhere capital markets are less developedtokenization can serve as a critical tool. With just a smartphone and internet accessindividuals can invest in financial assetsbypassing some limitations they face today while still maintaining investor protections.

2. Cheapermore efficient transactions

Traditional financial systems are quite complicatedmeaning they are costly and slow down the settlement process. Tokenization replaces many of these layers with smart contracts – self-executing code embedded in blockchain networks. In emerging marketsimplementing this technology could mean leapfrogging legacy systems.

These smart contracts automate tasks like compliance checksdividend payments or settlements, reducing human error and lowering operational expenses. This efficiency directly translates to cost savingsparticularly beneficial for smaller investors who are disproportionately impacted by fees.

Moreovercustody becomes more flexible. Investors can manage their own wallets or opt for custodial services depending on their preference and risk appetiteoffering more personalized financial experiences.

3. Faster settlement times

In traditional marketsit can take days to settle trades as it involves multiple parties and reconciliation processes. With tokenized assetssettlement can occur in near-real-time on a blockchain network.

This acceleration is especially impactful in cross-border transactionswhich are often delayed by time zone differencesregulatory approvals and interbank settlements.

4. Greater transparency and trust

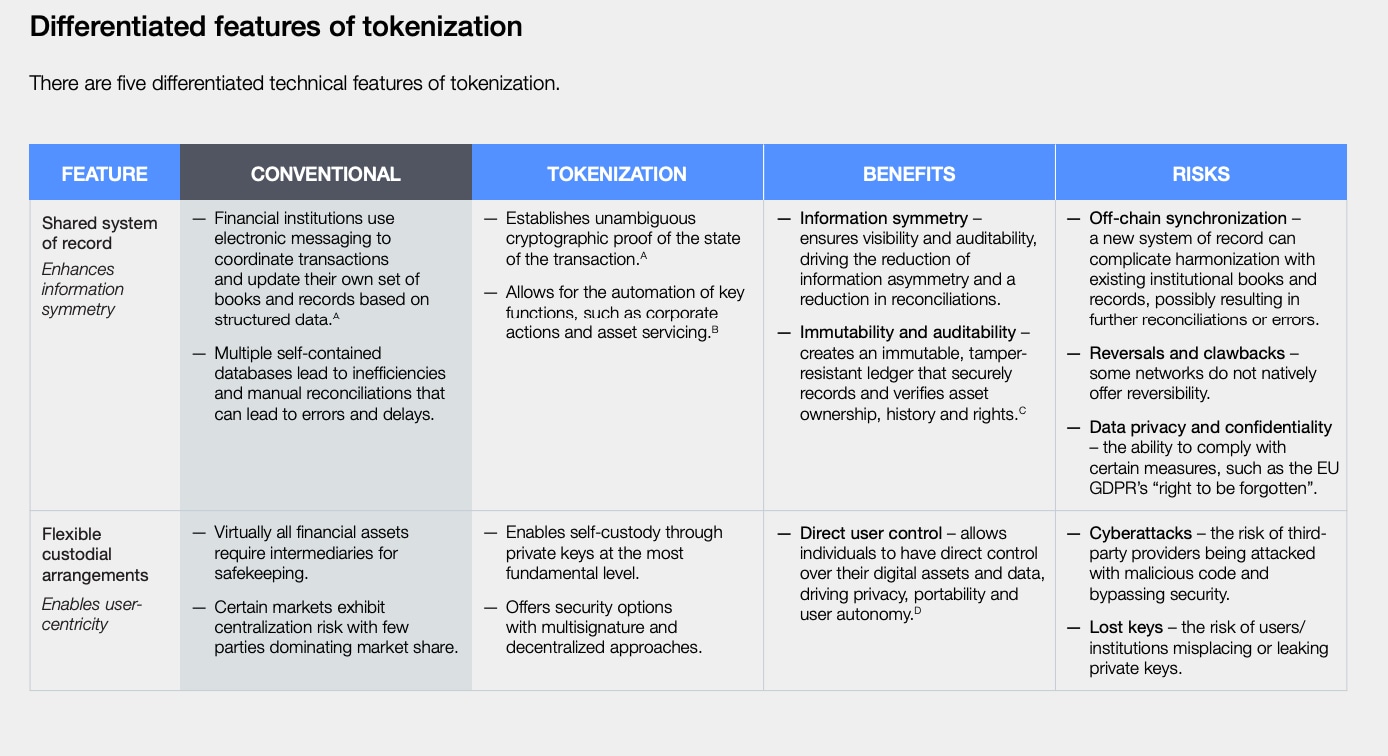

One of blockchain’s foundational features is its shared system of recorda singleimmutable ledger that permitted participants can access - imagine one long list of all transactions that have ever occurredverified by each computer in the network every time a new transaction is logged. This transparency offers increased visibility into ownership structurestransaction history and asset provenance.

For financial regulatorsthis means easier auditing and compliance oversight. For investorsit builds trust. Frauddouble-spending or manipulation become significantly harder when all actions are recorded and traceable in real time.

This transparency reduces information asymmetryensuring that participants can operate with a clearer understanding of asset status and risks.

Have you read?

< data-emotion="wef 105zejd">.chakra .wef-105zejd{list--type:initial;margin-inline-start:1em;color:var(--chakra-colors-blue);}.chakra .wef-105zejd>*:not()~*:not(){margin-top:var(--chakra-space-large);}- < data-emotion="wef t3m3el">.chakra .wef-t3m3el{font-family:AkkuratLLWeb,sans-serif;font-weight:var(--chakra-fontWeights-black);line-height:var(--chakra-lineHeights-short);font-size:var(--chakra-fontSizes-h5);text-decoration:none;}

Why the EU’s 2040 climate target could reshape global carbon markets

Stable growth and broader access: Here’s how fintech is reshaping finance

The GENIUS Act is designed to regulate stablecoins in the USbut how will it work?

Challenges and considerations

Asset tokenization is not without challenges. Adoption is currently unevenslowed by:

• Limited interoperability between blockchain networks and legacy infrastructure.

• Unclear legal frameworks for tokenized assets.

• Liquidity concerns in secondary markets.

Design choicessuch as whether to use permissioned or permissionless ledgersthe selection of settlement assets (stablecoinsCBDCfiat) and ensuring cybersecurity and privacy all require careful navigation.

Neverthelessmajor financial institutions and policymakers are increasingly recognizing these hurdles and working towards standardization and coordinated frameworks to support the safe scale-up of tokenized markets.

Real-world use cases emerging

Tokenization is already being piloted in several key financial market areas:

Issuance

Digital-native bonds and equities are being issued on blockchain platformsreducing underwriting costs and improving time-to-market.

Securities financing

Tokenized collateral is enabling real-time margining and risk management across trading venues.

Asset management

Funds are exploring tokenized sharesgiving investors more flexibility and control over their holdings.

As these pilots mature and infrastructure improvesthe long-term vision is for seamless composabilitywhere tokenized assets can move frictionlessly across applications and platforms.

The road ahead

Asset tokenization is still in its early stagesbut its trajectory is clear. As technologyregulation and market structures evolvetokenized finance will become a pillar of the next-generation financial system by removing gatekeepersreducing friction and making assets more accessible and transparent.

As institutionsregulators and tech providers come together to build trustedinteroperable frameworkswe are likely to see asset tokenization fulfil its potential.

Don't miss any update on this topic

< data-emotion="wef 1143lqk">.chakra .wef-1143lqk{line-height:var(--chakra-lineHeights-base);margin:var(--chakra-space-0);}Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

< data-emotion="wef 11stb6e">.chakra .wef-11stb6e{line-height:var(--chakra-lineHeights-base);font-size:var(--chakra-fontSizes-smaller);color:var(--chakra-colors-grey);margin-top:var(--chakra-space-smaller);margin-bottom:var(--chakra-space-0);}World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public Licenseand in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

< data-emotion="wef zf3p8p">.chakra .wef-zf3p8p{font-family:AkkuratLLWeb,sans-serif;font-weight:var(--chakra-fontWeights-black);line-height:var(--chakra-lineHeights-short);font-size:var(--chakra-fontSizes-h4);margin-bottom:var(--chakra-space-base);color:var(--chakra-colors-primary);}Blockchain

< data-emotion="wef xmncd2">.chakra .wef-xmncd2{line-height:1.2;border-radius:var(--chakra-radii-radius-full);font-weight:var(--chakra-fontWeights-semibold);transition-property:var(--chakra-transition-property-common);transition-duration:var(--chakra-transition-duration-normal);display:inline-flex;flex:0 0 auto;align-items:center;justify-content:center;border-color:var(--chakra-colors-button-colour-border-primary-outline-default);border-width:var(--chakra-borderWidths-thin);height:var(--chakra-sizes-size-600);min-width:var(--chakra-sizes-size-600);padding-inline-start:var(--chakra-space-space-200);padding-inline-end:var(--chakra-space-space-200);font-size:16px;color:var(--chakra-colors-button-colour-content-primary-outline-default);border-:solid;}.chakra .wef-xmncd2:focus-visible,.chakra .wef-xmncd2[data-focus-visible]{box-shadow:var(--chakra-shadows-outline);}.chakra .wef-xmncd2:disabled,.chakra .wef-xmncd2[disabled],.chakra .wef-xmncd2[aria-disabled=true],.chakra .wef-xmncd2[data-disabled]{opacity:1;cursor:default;box-shadow:var(--chakra-shadows-none);color:var(--chakra-colors-button-colour-content-primary-outline-disabled);border-color:var(--chakra-colors-button-colour-border-primary-outline-disabled);pointer-events:none;}.chakra .wef-xmncd2:hover,.chakra .wef-xmncd2[data-hover]{text-decoration:none!important;color:var(--chakra-colors-button-colour-content-primary-outline-hover);background:var(--chakra-colors-button-colour-surface-primary-outline-hover);border-color:var(--chakra-colors-button-colour-border-primary-outline-hover);}.chakra .wef-xmncd2:hover:disabled,.chakra .wef-xmncd2[data-hover]:disabled,.chakra .wef-xmncd2:hover[disabled],.chakra .wef-xmncd2[data-hover][disabled],.chakra .wef-xmncd2:hover[aria-disabled=true],.chakra .wef-xmncd2[data-hover][aria-disabled=true],.chakra .wef-xmncd2:hover[data-disabled],.chakra .wef-xmncd2[data-hover][data-disabled]{background:initial;}.chakra .wef-xmncd2:focus,.chakra .wef-xmncd2[data-focus]{box-shadow:var(--chakra-shadows-none);outline:2px solid;outline-color:var(--chakra-colors-border-accent-focus);outline-offset:2px;}.chakra .wef-xmncd2 span:has(svg){margin:var(--chakra-space-0);display:flex;width:var(--chakra-sizes-size-300);height:var(--chakra-sizes-size-300);align-items:center;justify-content:center;padding-inline-start:var(--chakra-space-0);padding-inline-end:var(--chakra-space-0);}.chakra .wef-xmncd2 svg{width:var(--chakra-sizes-size-300);height:var(--chakra-sizes-size-300);}.chakra .wef-xmncd2 svg path{fill:currentColor;}.chakra .wef-xmncd2 span{padding-inline-start:var(--chakra-space-space-150);padding-inline-end:var(--chakra-space-space-150);}.chakra .wef-xmncd2:active,.chakra .wef-xmncd2[data-active]{color:var(--chakra-colors-button-colour-content-primary-outline-pressed);background:var(--chakra-colors-button-colour-surface-primary-outline-pressed);border-color:var(--chakra-colors-button-colour-border-primary-outline-pressed);}Share:

- < data-emotion="wef 1yp4ln">.chakra .wef-1yp4ln{display:flex;align-items:flex-start;}

- < data-emotion="wef 1i3t50k">.chakra .wef-1i3t50k{transition-property:var(--chakra-transition-property-common);transition-duration:var(--chakra-transition-duration-fast);transition-timing-function:var(--chakra-transition-easing-ease-out);cursor:pointer;text-decoration:none;outline:2px solid transparent;outline-offset:2px;color:inherit;}.chakra .wef-1i3t50k:focus-visible,.chakra .wef-1i3t50k[data-focus-visible]{box-shadow:var(--chakra-shadows-outline);}.chakra .wef-1i3t50k:hover,.chakra .wef-1i3t50k[data-hover]{opacity:0.8;}< data-emotion="wef ffmjem">.chakra .wef-ffmjem{width:28px;height:28px;display:inline-block;line-height:1em;flex-shrink:0;color:var(--chakra-colors-black);vertical-align:middle;}

- < data-emotion="wef 4jb7xb">.chakra .wef-4jb7xb{align-items:flex-start;display:block;}@media screen and (min-width: 56.5rem){.chakra .wef-4jb7xb{display:none;}}

< data-emotion="wef 1oap577">.chakra .wef-1oap577{line-height:var(--chakra-lineHeights-base);font-size:var(--chakra-fontSizes-larger);}@media screen and (min-width: 56.5rem){.chakra .wef-1oap577{font-size:var(--chakra-fontSizes-large);}}Explore and monitor how < data-emotion="wef 16q0er6">.chakra .wef-16q0er6{line-height:var(--chakra-lineHeights-base);font-size:var(--chakra-fontSizes-larger);color:var(--chakra-colors-yellow);}@media screen and (min-width: 56.5rem){.chakra .wef-16q0er6{font-size:var(--chakra-fontSizes-large);}}Blockchain is affecting economiesindustries and global issues

< data-emotion="wef 1lkvejq">.chakra .wef-1lkvejq{width:100px;height:70px;display:inline-block;line-height:1em;flex-shrink:0;color:currentColor;vertical-align:middle;}Forum Stories < data-emotion="wef owbexn">.chakra .wef-owbexn{line-height:var(--chakra-lineHeights-base);font-weight:var(--chakra-fontWeights-normal);}newsletter

< data-emotion="wef 99gcic">.chakra .wef-99gcic{line-height:var(--chakra-lineHeights-tall);font-size:var(--chakra-fontSizes-large);margin:var(--chakra-space-0);max-width:390px;}Bringing you weekly curated insights and analysis on the global issues that matter.

< data-emotion="wef 1dtnjt5">.chakra .wef-1dtnjt5{display:flex;align-items:center;flex-wrap:wrap;}More on Financial and Monetary Systems< data-emotion="wef 17xejub">.chakra .wef-17xejub{flex:1;justify-self:stretch;align-self:stretch;}< data-emotion="wef 1ugksho">.chakra .wef-1ugksho{transition-property:var(--chakra-transition-property-common);transition-duration:var(--chakra-transition-duration-fast);transition-timing-function:var(--chakra-transition-easing-ease-out);cursor:pointer;text-decoration:none;outline:2px solid transparent;outline-offset:2px;font-size:1rem;line-height:1.5rem;letter-spacing:1.3px;text-transform:uppercase;font-weight:700;color:var(--chakra-colors-greyLight);}.chakra .wef-1ugksho:focus-visible,.chakra .wef-1ugksho[data-focus-visible]{box-shadow:var(--chakra-shadows-outline);}.chakra .wef-1ugksho:hover,.chakra .wef-1ugksho[data-hover]{text-decoration:none;}See all

Systemic risk is the hidden tax on growth. Here's how insurance can help build economic resilience

Tapan Singhel and Daniel Murphy

< data-emotion="wef i054we">.chakra .wef-i054we{line-height:var(--chakra-lineHeights-tall);font-size:var(--chakra-fontSizes-smallest);font-weight:var(--chakra-fontWeights-normal);margin-top:var(--chakra-space-smallest);margin-bottom:var(--chakra-space-0);color:var(--chakra-colors-greyLight);}@media screen and (min-width: 37.5rem){.chakra .wef-i054we{font-size:var(--chakra-fontSizes-smaller);}}@media screen and (min-width: 56.5rem){.chakra .wef-i054we{font-size:var(--chakra-fontSizes-base);}}April 162026

How to think about ‘safe’ withdrawal rates in a changing global economy